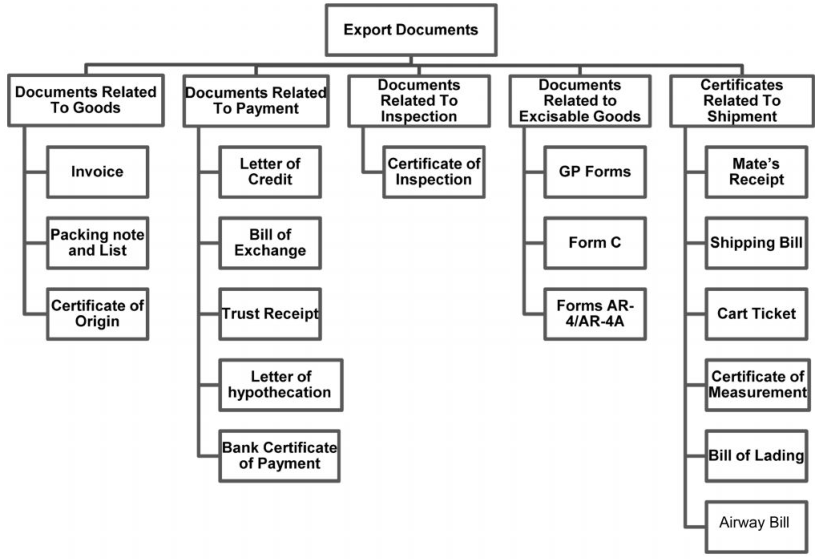

Some important documents in the foreign trade are as follows

Pro-forma Invoice

A pro forma invoice is much the same as a commercial invoice which, when used in international trade, represents the details of an international sale to customs authorities. A pro forma invoice is presented in the place of a commercial invoice when there is no sale between the sender and the importer, or if the terms of the sale between the seller and the buyer are such that a commercial invoice is not yet available at the time of the international shipment. A pro forma invoice is required to state the same facts that the commercial invoice would and the content is prescribed by the governments who are a party to the transaction.

Packing List

The packing list is a consolidated statement in a prescribed format, detailing how the goods have been packed. It is informative and itemizes the material in each individual package, such as a box or a carton. The packing list is an extension of the commercial invoice; as such it looks like a commercial invoice. The exporter or his/her agent—the customs broker or the freight forwarder-reserves the shipping space based on the gross weight or the measurement shown in the packing list. Customs uses the packing list as a check-list to verify the outgoing cargo (in exporting) and the incoming cargo (in importing). The importer uses the packing list to inventory the incoming consignment.

Commercial Invoice

A commercial invoice is a document used in foreign trade. It is used as a customs declaration provided by the person or corporation that is exporting an item across international borders. Although there is no standard format, the document must include a few specific pieces of information such as the parties involved in the shipping transaction, the goods being transported, the country of manufacture, and the codes for those goods. A commercial invoice must also include a statement certifying that the invoice is true, and a signature.

A commercial invoice is used to calculate tariffs, international commercial terms (like the Cost in a CIF) and is commonly used for customs purposes.

Certificate of Origin

A Certificate of Origin (often abbreviated to CO or COO) is a document used in international trade. It traditionally states from what country the shipped goods originate, but “originate” in a CO does not mean the country the goods are shipped from, but the country where the goods are actually made. A Certificate of Origin is issued by the local chambers of commerce

A preferential certificate of origin is a document attesting that goods in a particular shipment are of a certain origin under the definitions of a particular bilateral or multilateral free trade agreement (FTA). This certificate is required by a country’s customs authority in deciding whether the imports should benefit from preferential treatment in accordance with special trading areas or customs unions such as the European Union or the North American Free Trade Agreement (NAFTA) or before anti-dumping taxes are enforced.

The definition of “Country of Origin” and “Preferential Origin” are different. The European Union for example generally determines the (non-preferential) origin country by the location of which the last major manufacturing stage took place in the products production (in legal terms: “last substantial transformation”). Whether a product has preferential origin depends on the rules of any particular FTA being applied, these rules can be value based or tariff shift based. The FTA rules are commonly called “Origin Protocols”. The certificate of origin must be signed by the exporter, and, for a small number of countries, also validated by a Chamber of Commerce or local consulate of the destination country and notarized.

Shipping Bill/Bill of Entry

Shipping bill is required for seeking permission of customs to export goods by sea/air. It contains description of export goods, number and kind of packages, shipping marks and numbers, value of goods, the name of vessel, the country of destination etc.

Bill of entry is needed by importers for customs clearance and later to bank for verification.

ARE-I Form

This form is an application for the removal of excisable goods from the factory premises, for export purposes. For example, if you are exporting a product which doesn’t have an excise, you don’t have to fill this form.

The form has multiple copies, which are distributed to different authorities, including Customs, excise, etc. Earlier this form was known as AR 4

Mate’s receipt

After the cargo is cleared and handed over to the shipping company, Mate’s receipt is issued by the captain of the ship. It contains the name of the vessel, shipping line, port of loading, port of discharge, shipping marks and numbers, packing details, description of goods, gross weight, container number, and seal number.

Exchange Declaration form (GR/SDF Form)

The Reserve Bank of India has a prescribed GR form (SDF), a PP form and SOFTEX forms to declare the export transactions in order to monitor the foreign exchange. The GR form contains

- Name & address of exporter and value of goods

- Name and address of the authorized dealer through whom proceeds of exports have been or will be realized.

- Details of commission and discount due to foreign agent or buyer

The full export value of goods

Distribution of copies of GR Form

- GR forms are completed in duplicate and need to be submitted to the customs at the time of shipment

- After verification of goods and the value of goods, the GR form will be retained by the customs to be submitted to the RBI

- One of copy of GR form is obtained by the exporter from the concerned clearing agent.

- Exporter is obliged to give the duplicate copy of GR in less than 21 days from the date of shipment, to his authorized dealer (banker)

Statutory Declaration Form

Since customs department are getting computerized, to meet the requirement of Electronic Data Interchange, Statutory Declaration Form (SDF) is replacing GR form slowly. SDF carries the same provision as GR and is expected to replace GR form soon.

Post Parcel Form (PP)

PP form is used when goods are exported by post. It needs to be filled by the exporter and has to be first submitted to the banker for his necessary counter signature. It needs to be filled in 3 copies. The bank returns the PP form to the exporter for submitting it to the post office along with the parcel. The post office forwards a copy to the RBI after dispatch of goods. The other copy goes to the authorized dealer within 21 days, to whom the exporter submits for collection.

SOFTEX Forms

All exports of software/audio/video/television software is declared on SOFTEX form. The SOFTEX form in triplicate is submitted to the designated official of Department of Electronics of Government of India at the Software Technology Parks of India (STPIs) or at the Free Trade Zones (FTZs) or Export Processing Zones (EPZs). After signing by the official, one copy is sent to RBI, one retained by the official, and one given to the exporter

Bill of exchange

It is “an instrument in writing, containing an order, signed by the maker, directing a certain person to pay a certain sum of money only to the order of a person to bearer of the instrument”.

It is commonly known as a draft. The bill of exchange is a negotiable instrument. A negotiable instrument is a document guaranteeing the payment of a specific amount of money, either on demand, or at a set time. According to the Negotiable Instruments Act, 1881 in India there are just three types of negotiable instruments i.e., promissory note, bill of exchange and cheque.

Types of Bills of exchange

Sight Draft

When the importer (drawee) makes payment immediately upon presentation of the draft, it is called sight draft. The corresponding term of payment is referred to as Delivery against Payment (D/P)

Usance Draft

Used when exporter gives credit to the importer. A draft may be drawn as per period of credit i.e. 30 days/60 days, after it is presented to the importer. On due date, the payment will be made to the bank who then forwards it to the exporter’s bank.

When payment is received in advance, no bill of exchange is required.

Inspection Certificate

Inspection certificate is required by some countries to get the specifications of goods being shipped and is normally given by a government agency or some independent testing organizations.

Bill of Lading

A bill of lading (BL – sometimes referred to as BOL or B/L) is a document issued by a carrier to a shipper acknowledging that specified goods have been received on board as cargo for conveyance to a named place for delivery to the consignee who is usually identified. A through bill of lading involves the use of at least two different modes of transport from road, rail, air, and sea. The term derives from the verb “to lade” which means to load a cargo onto a ship or other form of transportation. A bill of lading can be used as a traded object.

B/L is generally made out in sets of three originals. All originals are duly signed by the master of the ship or the agent of the shipping company and all the originals are equally valid for taking the delivery of the goods.

B/L is the legal document for any dispute resolution and contains the following information

- Name of the shipping company

- Flag of nationality

- Shipper’s name

- Order and notify party

- Description of goods

- Gross/net/tare weight

- Freight rate/measurements and weight of goods/total freight

Airway Bill

Air Waybill (AWB) or air consignment note refers to a receipt issued by an international airline for goods and an evidence of the

contract of carriage, but it is not a

document of title to the goods. Hence, the AWB is

non-negotiable.

The first three letters of the Airway Bill Number normally represents the airline code. For Example: 176 for emirates, 125 for British Airways etc.

There are several purposes that an air waybill serves, but its main functions are

- Contract of Carriage. Behind every original of the AWB are conditions of contract for carriage

- Evidence of Receipt of Goods

Insurance Certificate

Insurance certificate is to assure the consignee that goods will be covered for loss or damage to the cargo during transit.

Consular Invoice

Consular invoice is a document required by certain countries, that needs to be submitted to the embassy of the concerned country. It is also known as certificate of origin and is required to be signed by the official in the embassy of the importing country, to enable the importer’s country to collect accurate and authenticated information about the value, volume, quantity, source etc of the import for assessing import duties and for other statistical purposes.